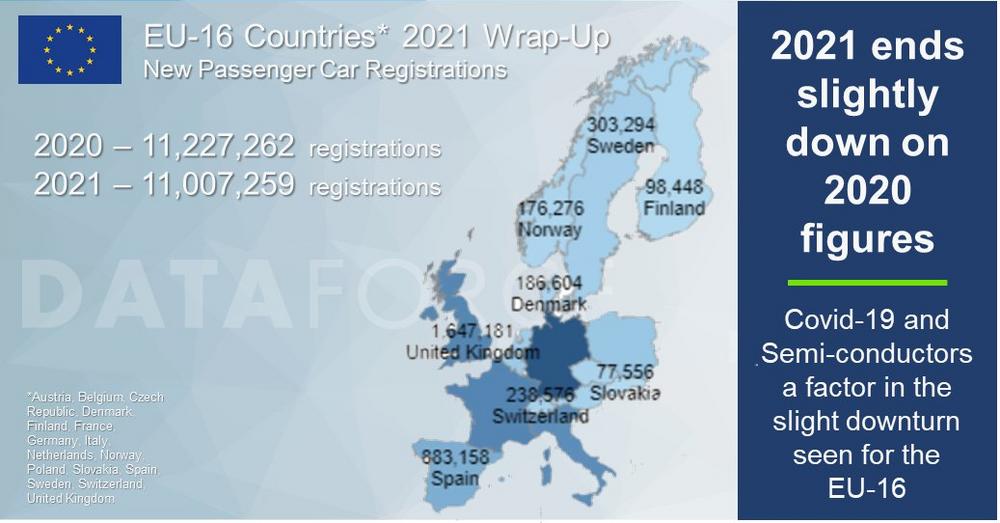

The EU16 had both ups and downs in 2021 – positive and negative ones.

So which “ups” & “downs” were positive?

Well, there is of course the most obvious “up” coming from fuel type. The BEVs, PHEVs and Hybrids all showed record volumes, with the BEVs and PHEVs both exceeding 1,000,000 registrations each in 2021 or + 62.7% and + 67.8% respectively over their 2020 figures. True Fleets increased their PHEV volume by 186,000 units over 2020, but it was a staggering +244,000 for BEVs from Private registrations which saw the largest volume increase of any fuel type and channel.

Positive “downs” come from the CO2 output of the EU-16 countries. With the average emissions being 116 grams based on WLTP, this was an average CO2 reduction of 19 grams over 2020 and shows the positive impact of the alternative fuel type increases and ICE engine decreases. Winner in terms of reductions goes to Norway which dropped its CO2 output by an impressive 40% and putting this into context actually makes this even more staggering! The previous year was already only 47 grams, meaning for 2021 they have managed an output of just 28 grams! Next nearest competitor was Sweden, which also dropped 20% to finish on 90 grams. Other countries to reach the sub 100 grams for 2021 were Denmark with 93 grams and the Netherlands with 95 grams, so it truly is the Scandinavians leading the way.

Which negative “ups” & “downs” did we find in the EU16?

Sticking with CO2 for the EU-16, there is one country which showed an increase over 2020 output, and that was Slovakia. It has moved from 149 grams in 2020 to 160 grams in 2021. Looking at the market channels, we see that the biggest increases came from the tactical channels of RAC and Dealer/Manufacturer which showed increase of 12% and 10% respectively.

Given their status as leading passenger car manufacturer VW showed a slight contraction finishing down by 70,000 registrations or 0.4% market share. However, what should be quickly pointed out is their volumes increases in BEVs and PHEVs over 2020 registrations. A growth by 65,900 units account for a little over 7.7% of all the increases seen in the EU16.

Negative or Positive “ups” & “downs” you decide?

SUV segments continue to gain in both volume and market share, with SUV Compact now accounting for 20% market share of all new car registrations and gaining 12.1% in volume over 2020. PC Small and PC Compact are the opposite and continue to drop in volume with losses of 7.5% and 13.7% respectively. Their corresponding market shares also dropped by 1% and 2% respectively.

Now are the future small and compact passenger cars with BEV or PHEV powertrains eventually going to swing the tide back in their favour and regain that market share? Will SUVs as one of the highest emitters of CO2, especially with pure ICE engines, hold back the possible quicker achievement of CO2 reductions?

With chip shortages easing, alongside COVID restrictions, 2022 is certainly shaping up to be an interesting year for the EU-16.

Dataforce is the leading provider of fleet market data and automotive intelligence solutions in Europe. In addition, the company also provides detailed information on sales opportunities for the automotive industry, together with a wide portfolio of information based on primary market research and consulting services. The company is based in Frankfurt, Germany.

Dataforce Verlagsgesellschaft für Business Informationen mbH

Hamburger Allee 14

60486 Frankfurt am Main

Telefon: +49 (69) 95930-0

Telefax: +49 (69) 95930-333

http://www.dataforce.de

Telefon: +49 (69) 95930-253

Fax: +49 (69) 95930-333

E-Mail: richard.worrow@dataforce.de

Junior Marketing Manager

Telefon: +49 (69) 95930-353

Fax: +49 (69) 95930-333

E-Mail: claudia.articek@dataforce.de

![]()